by Adrienne Markes

On Apr 26, 2017

Listed in Blog>Buyer Info, Blog>Market Condition, Blog>Seller Info

On Apr 26, 2017

Listed in Blog>Buyer Info, Blog>Market Condition, Blog>Seller Info

A nicely upgraded detached home comes on the market in mint condition listed FOR SALE at $650,000. During the initial weekend, the open house is a total success with buyers bumping into each other to see the home. By Monday morning, the listing agent is sorting through five offers to purchase the home. By the week’s end, the seller is able to come to an agreement and accepts a full price offer that closes in 30-days.

A beautiful upgraded luxury homes comes on the market with an entertainer’s yard listed FOR SALE at $1.6 million. Seven different buyers tour the home in the initial week. Quite a few people come through the weekend open house. The first week’s activity is solid, yet there are no offers generated. It is not until nearly hitting the three-month mark on the market when the sellers are entertaining their first offer. There had been some interest prior, but nobody was willing to step up and write an offer to purchase. A few days later, after back and forth negotiations, the seller comes to an agreement and accepts an offer for $30,000 less than what they were asking and closes in 60-days.

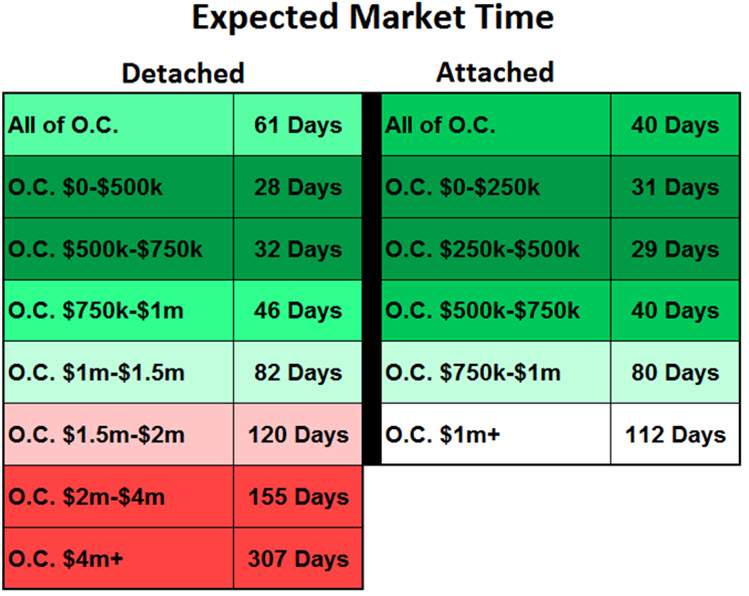

These two scenarios are both taking place right here in Orange County and are typical for their specific price ranges. Yes, the market is HOT, but in the high range, it takes longer to sell a home. The “FLAVOR” of the market really depends upon the price point of a home.

The market is sizzling hot for homes priced below $750,000. That price range gets the most press and it is what everybody is talking about in discussing Orange County housing. When you hear about multiple offers within days and lines of people touring the open house, chances are it is a home in the lower end of the market. The lion’s share of all closed sales in 2017, two-thirds took place below $750,000. It is a majority of today’s market, yet there are not enough on the market today. It currently accounts for only 37% of the active listing inventory.

The $750,000 to $1 million price range is still hot, but, on average, it takes a couple of more weeks to negotiate a deal compared to the lower ranges. Condominiums in this range need to price carefully. There just are not as many buyers looking to purchase an attached home priced above three-quarters of a million dollars.

Above $1 million, the market decelerates quite a bit. The expected market time is still less than 90-days for homes priced between $1 million to $1.5 million, but they are not flying off the market with buyers tripping over themselves to purchase. We are also seeing multiple price drops before a property in this ranges actually goes under contract.

Above $1.5 million, it’s a totally different ballgame, ranging from an expected market time of 4 months to nearly a year. There simply are not enough luxury buyers, but there are certainly plenty of competing sellers.

Regardless of the price range, from now through August, there will be a lot more homes coming on the market and the active inventory will continue to grow. As the supply of homes grows and demand stays relatively the same, the expected market time will grow as well. More homes coming on the market means more competition. In order to find success at ALL price points, it is imperative that sellers carefully price their homes according to their Fair Market Values. Stretching the asking price results in wasted market time and sitting on the market with no success. Many sellers will fall victim to overpricing and will not achieve their objective until they correct their asking price with a reduction more in alignment with their true Fair Market Value.